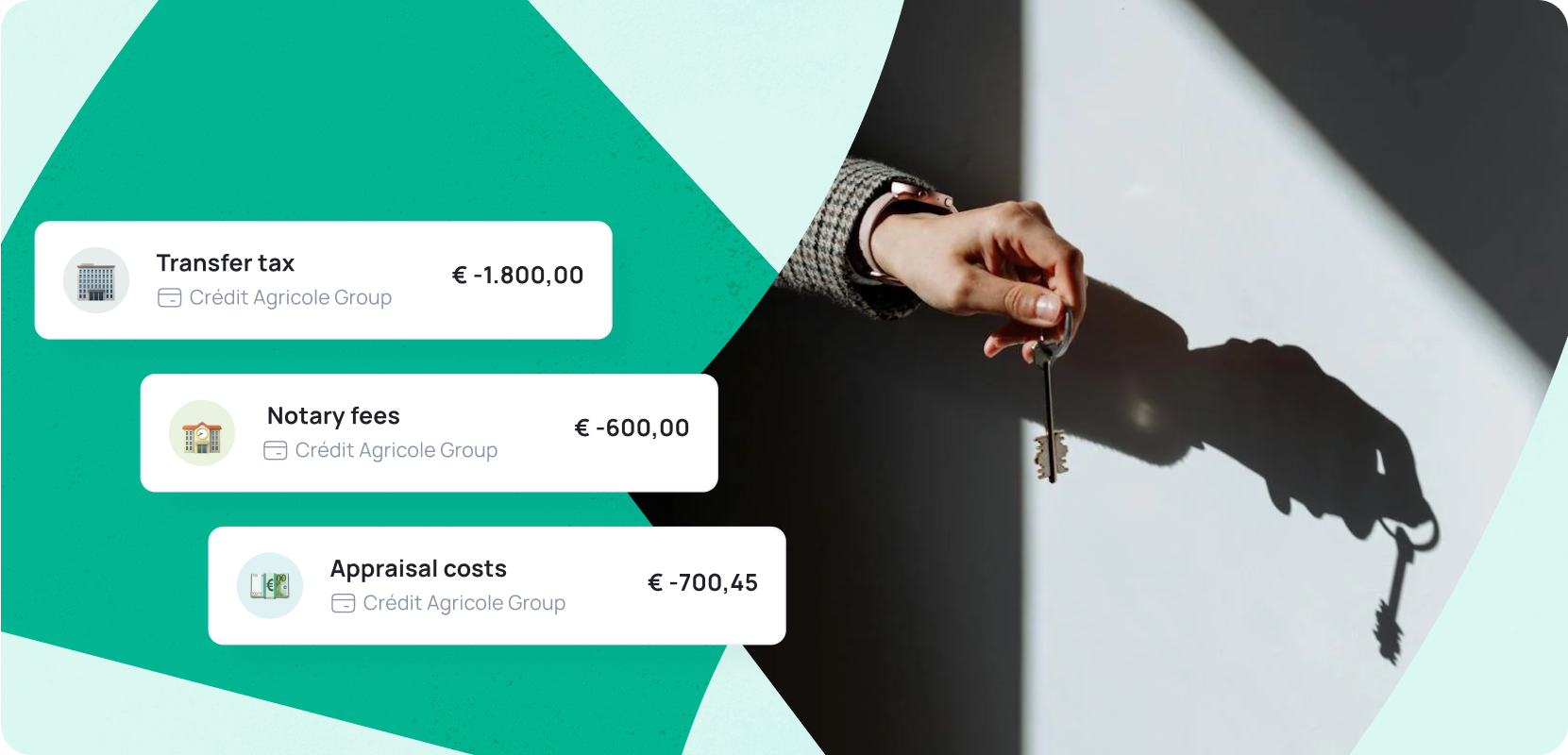

1. Transfer Tax

One of the largest additional costs when buying a house is the transfer tax. This tax, calculated as a percentage of the purchase price, often forms the bulk of the buyer's costs. In the Netherlands, the transfer tax is 2% of the purchase price.

Free Tip: If you are under 35 and buying your first home, you do not have to pay transfer tax. In 2025, this exemption applies to homes costing up to €525,000. This can save you a significant amount. Check current conditions with the Dutch Tax Authorities or your notary.

2. Notary Fees

Notary fees are another mandatory part of the buyer's costs. The notary prepares the deed of transfer and the mortgage deed, and ensures registration with the Dutch Land Registry. These costs vary by notary and are generally unrelated to the property’s purchase price.

- Indicative Cost for Deed of Transfer: €600–€900

- Indicative Cost for Mortgage Deed: €600–€900

Free Tip: Compare notary fees, as prices can vary significantly.

3. Appraisal Costs

A property appraisal is often required when applying for a mortgage. An appraiser determines the property’s market value, which the bank uses to determine the loan amount. Appraisal costs vary based on the type, value, and location of the property, as well as the appraiser.

- Average Cost: €550–€1,000

4. Mortgage Advice and Brokerage Costs

When securing a mortgage, you will need to pay for advice and brokerage services. A mortgage advisor helps you find the right mortgage and guides you through the process.

- Average Cost: €1,500–€3,000

Free Tip: Request quotes from multiple advisors and banks to compare rates and services, potentially lowering your buyer’s costs.

5. National Mortgage Guarantee (NHG) Costs

If eligible, you can opt for the National Mortgage Guarantee (NHG), which provides a safety net if you’re unable to pay your mortgage due to circumstances like unemployment or divorce. In 2025, the premium is 0.4% of the mortgage amount, and the NHG limit is €450,000.

Free Tip: The NHG limit is reviewed annually. Ask your mortgage advisor about the current limit and conditions to see if you qualify.

Examples:

- Flat (mortgage €220,000): 0.6% of €220,000 = €1.320

- Family Home (mortgage €400,000): 0.6% of €400,000 = €2.400

- Villa: Not applicable, as it exceeds the NHG limit.

6. Structural Survey 🛠️

A structural survey assesses the technical condition of a property, identifying defects or risks. Though not mandatory, it is highly recommended—especially for older homes. This investment can prevent unexpected (and costly) surprises after purchase. This investment can therefore save you money in the long run.

- Average Cost: €350–€600

7. Real Estate Agent Fees

If you hire a real estate agent, you will need to pay their fees. A real estate agent assists with finding the right home, making an offer, and negotiating. The fee is typically 1%–2% of the purchase price.

Examples (1.5% Commission):

- Flat (€220,000): 1.5% of €220,000 = €3,300

- Family Home (€400,000): 1.5% of €400,000 = €6,000

- Villa (€900,000): 1.5% of €900,000 = €13,500

8. Bank Guarantee

When buying a house, you are often required to pay a deposit of 10% of the purchase price. If you do not have this amount readily available, you can arrange a bank guarantee. This typically costs around 1% of the guarantee amount.

Examples:

- Flat (10% of €220,000 = €22,000): 1% = €220

- Family Home (10% of €400,000 = €40,000): 1% = €400

- Villa (10% of €900,000 = €90,000): 1% = €900

Other Costs

In addition to the costs mentioned above, there are other expenses to consider when buying a house, such as moving costs, renovations, and furnishing (e.g., new furniture and flooring). You will also need to take out new insurance policies, such as home insurance and life insurance.

Total Buyer’s Costs 💰

To estimate the total buyer’s costs, you can generally assume 5%–6% of the purchase price.

Examples:

- Flat (purchase price €220,000): 5%–6% = €11,000–€13,200

- Family Home (purchase price €400,000): 5%–6% = €20,000–€24,000

- Villa (purchase price €900,000): 5%–6% = €45,000–€54,000

Grassfeld: Gain Insight Into Your Expenses with a Free App

Are you planning to buy a house and want a clear overview of the additional costs? Grassfeld can help. The free app automatically categorizes your expenses, so you can see exactly where your money goes. Additionally, you can set savings goals and create budgets in the app. With Grassfeld, you will always have control over your finances. Download the app now from your app store!